For over a century, auto insurance has been built on a simple, human-centric premise: who’s at fault? The driver. But what happens when the “driver” is a complex web of software, sensors, and algorithms? That’s the multi-billion-dollar question the industry is grappling with as autonomous and semi-autonomous vehicles shift from sci-fi to showroom.

The transition won’t be a light switch flip. It’ll be a messy, decades-long dance between human-controlled cars, cars with serious assists, and truly driverless vehicles. And insurance, that necessary piece of paper in your glovebox, is in for a total reinvention. Let’s dive in.

From Driver Risk to Product Liability: The Core Shift

Here’s the deal. Traditional insurance assesses driver risk—your age, your record, how many miles you drive. In a fully autonomous world, the risk profile migrates. It moves from the person in the seat (who might just be a passenger) to the manufacturers and software developers.

Think of it like this: you don’t buy “pilot insurance” when you board a commercial flight. The airline and aircraft manufacturer carry that liability. A similar model could emerge for robotaxis and Level 5 autonomous vehicles. The insurance policy becomes less about you and more about the cybersecurity of the car’s systems, the reliability of its lidar, and the integrity of its millions of lines of code.

The Murky Middle: Semi-Autonomous Headaches

Now, the real near-term challenge—and it’s a big one—is the semi-autonomous phase. Cars with Tesla’s Autopilot, GM’s Super Cruise, or similar systems are already here. They create a dangerous gray area in liability. Is the human “monitoring” the system ultimately responsible, or is the manufacturer when its system fails?

Insurance claims are already getting more complex, requiring deep forensic analysis of vehicle data. This period might actually see insurance costs increase for some models, as insurers price in the uncertainty and the high cost of repairing sensor-laden bumpers. It’s a classic case of technology outpacing regulation and, frankly, our own human complacency.

How Insurance Models Will Adapt (It’s Not Just Cheaper)

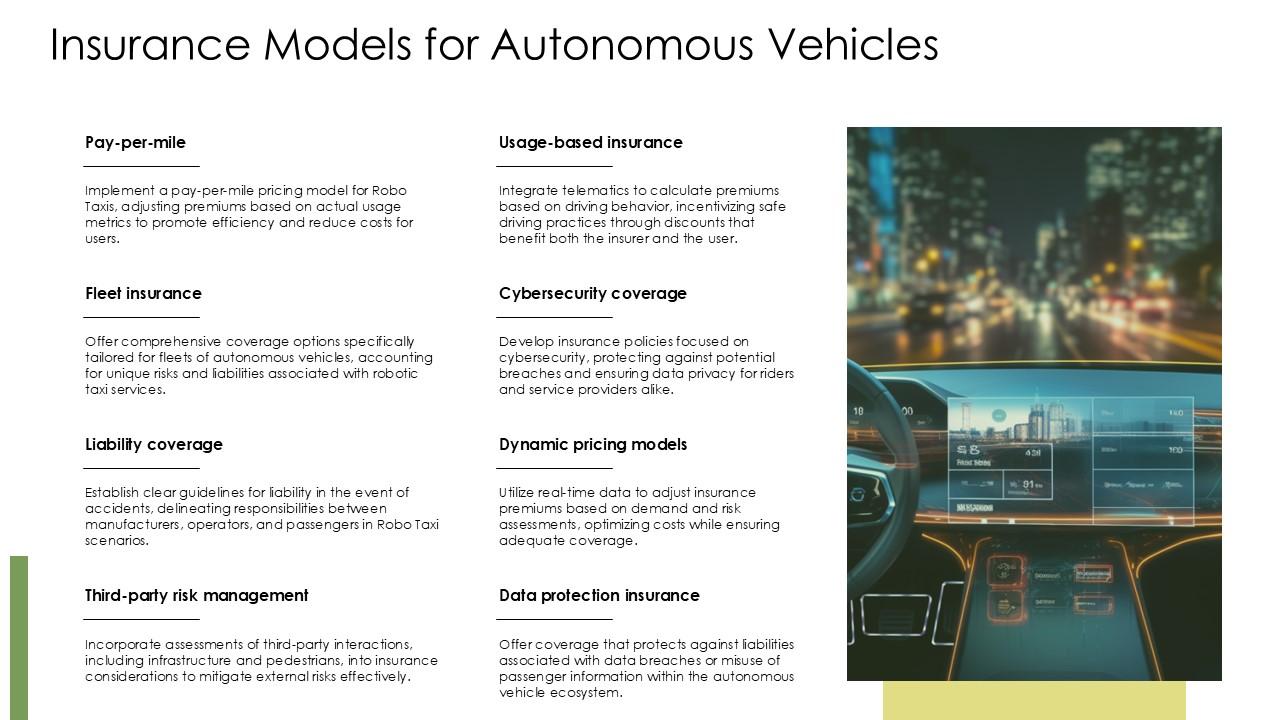

Everyone assumes autonomous vehicles mean cheaper insurance. Probably, in the long run. But the path there involves entirely new models. Here’s what’s taking shape:

- Usage-Based Insurance (UBI) on Steroids: Today’s telematics track your braking and mileage. Tomorrow’s will track autonomous system engagement. Did you override the system safely? Did you take control in a construction zone? Your premium could be based on how well you interact with the car’s AI.

- Manufacturer-Direct Policies: Carmakers like Volvo and Mercedes have already signaled they’ll accept liability when their full self-driving systems are engaged. They might just bundle the insurance into the car’s purchase price or subscription fee. You’d essentially be buying a car and its insurance as one package.

- Mobility-as-a-Service (MaaS) Coverage: When you summon a robotaxi, who insures that trip? The fleet operator (Waymo, Cruise, etc.) likely will, folding it into your ride cost. Personal auto insurance could become far less common if ownership plummets.

The Data Goldmine and New Players

Autonomous vehicles are data factories. This information—how the car perceives the world, makes decisions, and handles edge cases—is incredibly valuable. Whoever controls this data has a massive advantage.

This is why we’re seeing tech giants and auto manufacturers themselves eyeing the insurance space. They have the data. Traditional insurers risk becoming mere underwriters if they can’t access or interpret the vehicle data streams. Partnerships are forming, but the power balance is shifting.

| Traditional Model | Transitional Model | Future Model (Full Autonomy) |

| Insures the human driver | Hybrid liability (human + OEM) | Insures the vehicle technology & operator |

| Based on driver history & demographics | Based on telematics & system usage data | Based on software safety & fleet performance |

| Claim: human error determination | Claim: complex data forensics | Claim: product liability/cyber incident |

Real-World Hurdles on the Road Ahead

Sure, the destination seems clear. But the road is full of potholes. First, there’s the regulatory patchwork. Laws vary wildly by state and country. A uniform framework for liability and insurance minimums for AVs is… well, it’s a distant dream, honestly.

Then there’s the cybersecurity threat. A hacked fleet of autonomous vehicles is an insurer’s nightmare scenario. Policies will need to cover digital ransom events, mass software recalls, and sensor spoofing. It’s a whole new category of risk.

And let’s not forget the human factor—the mixed traffic period. How does an autonomous vehicle’s pristine driving record stay pristine when a human-driven car plows into it? Determining fault in these interactions will keep claims adjusters and lawyers busy for years.

What This Means for You, the Driver (For Now)

So, while we wait for the robotaxis, what should you do? If you’re buying a car with advanced driver-assist systems, ask questions. Understand exactly what the system does and, crucially, what it doesn’t do. Your vigilance is still the most important safety feature.

Consider usage-based insurance now. Getting comfortable with telematics can prepare you for the more data-intensive policies of the near future. And finally, stay informed. The fine print on your policy—especially around aftermarket parts and who repairs those expensive sensors—is about to get a lot more important.

The Final Turn: A Safer, But Different, Landscape

The ultimate promise of autonomous vehicles is a dramatic reduction in accidents. That’s the north star. In that world, the insurance industry shrinks in one way but morphs into something else—a backstop for technological failure rather than human error.

It’s a future where the concept of a “no-fault accident” might take on a completely new meaning. The “fault” may lie in a line of code, a missed software update, or a sun flare that confused a sensor. The relationship between car, human, and insurer is being quietly, irrevocably rewritten in real-time. And we’re all along for the ride, whether we’re driving or not.